By 2025, more than 40 biosimilars have been approved in the U.S. - drugs designed to be nearly identical to expensive biologic medicines like Humira, Enbrel, and Lantus. They’re proven safe, effective, and cost 10% to 33% less. But if you’re a patient trying to get one, you might as well be fighting a maze. Insurance companies aren’t making it easy. In fact, they’re often making it harder than getting the original brand-name drug.

Why Biosimilars Are Still Hard to Get

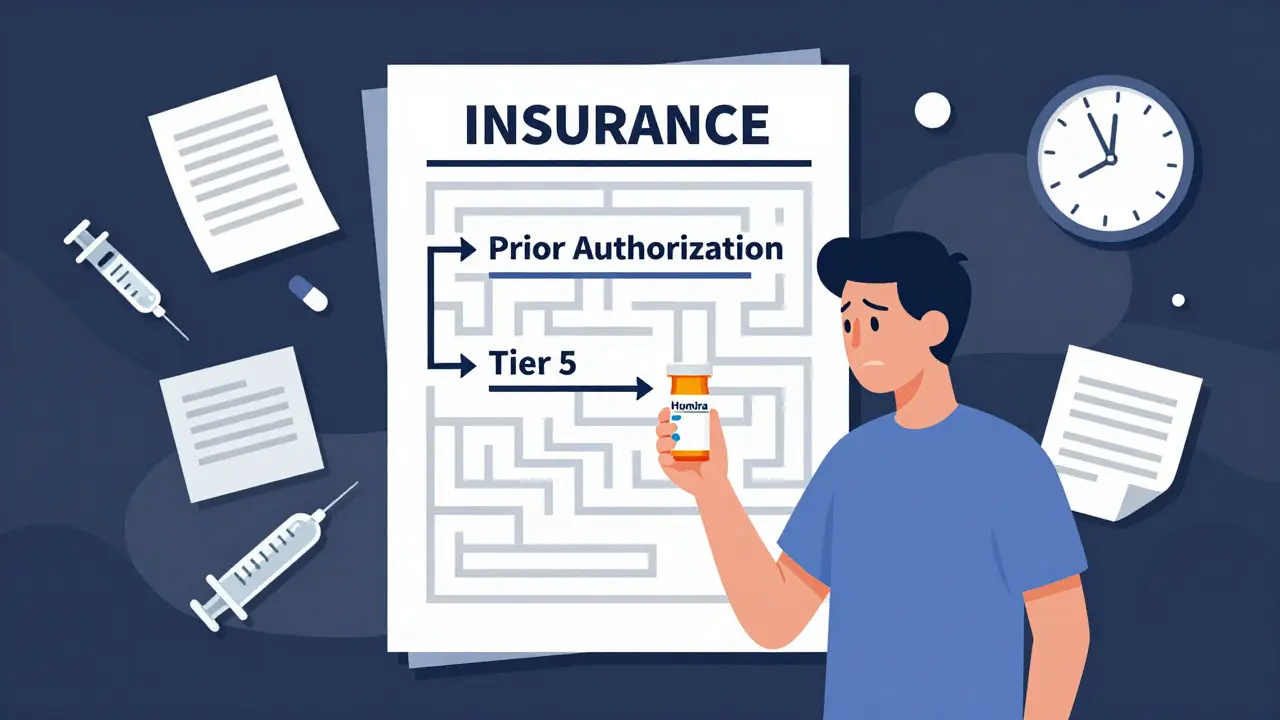

Biosimilars aren’t generics. They’re not simple chemical copies like the ones you get for blood pressure pills. They’re made from living cells - complex, expensive to produce, and tricky to replicate exactly. That’s why they’re called biosimilars, not generics. The FDA approved the first one, Zarxio, back in 2015. Since then, over 70 have been cleared. But only about 40 are actually on the market. And even when they are, insurance plans rarely make them the obvious choice.Take Humira, the best-selling drug in U.S. history. It costs around $5,000 a month. Eight biosimilars now exist as cheaper alternatives. Yet, according to JAMA Network data from June 2024, only half of Medicare Part D plans cover even one of them. And when they do? They’re usually placed on the same high-cost tier as Humira. That means you pay the same out-of-pocket price - $1,150 to $1,200 a month - whether you get the brand or the biosimilar. Where’s the incentive to switch?

Prior Authorization: The Hidden Gatekeeper

Nearly every insurance plan that covers biosimilars also requires prior authorization. That’s a form your doctor has to fill out, often with lab results, treatment history, and proof you’ve tried other drugs first. It can take 3 to 14 days to get approved. For someone with rheumatoid arthritis or Crohn’s disease, waiting two weeks for treatment isn’t just inconvenient - it’s dangerous.Here’s the kicker: 98.5% of plans require prior authorization for both Humira and its biosimilars. Not one plan makes the biosimilar easier to get. In fact, some require you to try the biosimilar first before they’ll approve the brand-name drug. That’s called step therapy. A case study in Rheumatology Advisor showed a patient with severe arthritis waited 28 days because their insurer forced them to try a biosimilar first. The patient’s symptoms worsened. Their doctor had to appeal. It was exhausting.

Doctors are spending 3 to 5 hours a week just handling these requests, according to a 2024 survey by the Alliance for Patient Access. That’s time they could be seeing patients - not chasing paperwork.

Tier Placement: The Real Barrier

Insurance plans use tiers to control costs. Tier 1 is cheap generics. Tier 4 or 5 is specialty drugs - the expensive ones like biologics. Biosimilars almost always land in Tier 4 or 5. That means you pay a percentage of the drug’s price, not a flat copay. If the drug costs $5,000, and your coinsurance is 33%, you pay $1,650 a month. Even if the biosimilar is $500 cheaper, you’re still paying $1,500. That’s not savings - that’s a penalty.According to the Center for Biosimilars, only 1.5% of plans put biosimilars on a lower tier than the reference drug. That’s almost zero. Meanwhile, Medicare Part D formularies in 2025 placed Humira and its biosimilars on the exact same tier - 99% of the time. No preference. No discount. No reward for choosing the cheaper option.

And it’s worse for insulin biosimilars. Eight are approved. Less than 10% of Medicare plans cover them. Even though insulin costs can be life-or-death for diabetics, insurers are still blocking access to cheaper versions.

Why PBMs Are Playing Hardball

The real power behind these rules isn’t the insurance company - it’s the pharmacy benefit managers (PBMs). These are the middlemen that negotiate drug prices and decide what goes on formularies. Express Scripts, OptumRx, and CVS Caremark control most of the market. And they’ve changed tactics.In 2025, Express Scripts completely removed Humira from all its commercial formularies. Not just restricted - gone. If you want Humira, you’re out of luck. But they put multiple biosimilars on preferred tiers with lower coinsurance (25% instead of 33%). That’s not an accident. It’s a strategy: force patients to switch by removing the brand entirely.

Other PBMs are following. This is a shift from passive coverage to active exclusion. But here’s the problem: it only works if the biosimilar is affordable and accessible. If patients can’t afford the coinsurance, or if the prior authorization takes weeks, they still won’t get treated. And if their doctor doesn’t know which biosimilars are covered, they’ll just prescribe the brand - because it’s easier.

Patients Pay the Price

The numbers don’t lie. Medicare Rights Center found that when biosimilars and Humira are on the same tier, patients pay almost the same amount out of pocket. The biosimilar might be $50 cheaper per month - but that’s not enough to motivate a change. Especially when you’re already paying $1,200 a month.For many, that’s not just expensive - it’s unaffordable. One patient in Texas skipped doses to stretch her Humira supply. She ended up in the ER. Her insurance didn’t care. The biosimilar was available. But her plan didn’t make it easy to get.

And it’s not just Medicare. Commercial plans are doing the same. UnitedHealthcare, Cigna, and Centene still don’t cover any insulin biosimilars - even though they’ve been approved for years. The message? We’ll cover the expensive drug. But the cheaper version? Not yet.

What’s Changing - and What’s Not

There’s some progress. The Congressional Budget Office estimates biosimilars could save the U.S. healthcare system $54 billion over the next decade. CMS started requiring plans to report biosimilar coverage in 2024. And in 2025, the Office of Inspector General pushed for stricter rules on tier placement.But change is slow. The FDA has approved dozens of biosimilars. The science is solid. The savings are real. The problem isn’t the drug - it’s the system. Insurance rules are designed to protect revenue, not patients.

Some PBMs say tier alignment reflects clinical equivalence. But that’s not true. Clinical equivalence doesn’t mean financial equivalence. If two drugs work the same, why should one cost twice as much out of pocket? The FTC has called these practices anti-competitive. Former FDA Commissioner Dr. Scott Gottlieb said they violate the spirit of the law meant to bring down biologic prices.

What Patients Can Do

You’re not powerless. Here’s what you can do:- Ask your doctor: "Is there a biosimilar available for my drug?" Don’t assume they know.

- Call your insurer. Ask: "Is the biosimilar on a lower tier than the brand?" If not, ask why.

- Request a formulary exception. If your doctor says you need the brand, they can appeal.

- Check your plan’s formulary online. Look up the drug name and see what tier it’s on.

- If you’re on Medicare, use the Medicare Plan Finder. Compare plans during open enrollment - coverage changes every year.

It’s not easy. But if you don’t ask, you won’t get it.

The Road Ahead

The U.S. biosimilar market grew to $15.3 billion in 2024 - up from $12 billion in 2022. But market share is still only 23% for adalimumab drugs. In Europe, it’s over 80%. Why? Because European insurers actively push biosimilars to the front of the line. They put them on lower tiers. They waive prior authorization. They let pharmacists substitute them automatically.The U.S. could do the same. But right now, the system is broken. Insurance companies aren’t saving money - they’re just shifting costs to patients. And the people who need these drugs the most are the ones paying the highest price.

If you’re paying over $1,000 a month for a biologic, you deserve better. The science says biosimilars work. The numbers say they save money. The question is: will insurance ever make it easy for you to get them?

Why aren’t biosimilars cheaper for patients if they cost less to produce?

Biosimilars are cheaper for insurers to buy - but insurance plans often place them on the same high-cost tier as the brand-name drug. That means patients pay the same coinsurance - usually 25% to 33% of the drug’s list price. Even if the biosimilar costs $500 less, the patient’s out-of-pocket bill barely changes. Without lower-tier placement, there’s no financial incentive to switch.

Can pharmacists substitute a biosimilar for the brand-name drug automatically?

Only if the biosimilar is designated as "interchangeable" by the FDA. As of 2025, only a few biosimilars - like adalimumab-adbm (Cyltezo) - have this status. But even then, substitution is limited to low-concentration versions of Humira, which are rarely prescribed. Most biosimilars require a new prescription. Pharmacists can’t swap them in without doctor approval.

Do all insurance plans cover biosimilars?

No. As of 2025, only about half of Medicare Part D plans cover any biosimilar for Humira. For insulin biosimilars, coverage drops below 10%. Many commercial insurers, including UnitedHealthcare and Cigna, still don’t cover any insulin biosimilars. Coverage varies wildly by plan, drug, and state.

Why do insurers require prior authorization for biosimilars if they’re approved by the FDA?

FDA approval means the drug is safe and effective - not that it’s affordable or preferred. Insurers use prior authorization to control costs and steer patients toward drugs that give them rebates or discounts. Even if a biosimilar is cheaper, insurers may still require proof you’ve tried other drugs first. It’s a financial tactic, not a medical one.

Can I switch from a brand-name biologic to a biosimilar without my doctor’s approval?

No. Even if your insurer approves the biosimilar, you still need a new prescription from your doctor. Unlike generic pills, biosimilars are not automatically substitutable. Your doctor must write a new order. Some states allow pharmacist substitution for interchangeable biosimilars, but that’s rare and limited to specific drug formulations.

Are biosimilars covered under Medicare Part D?

Yes - but inconsistently. In 2025, 78% of Medicare Part D plans covered at least one biosimilar for Humira, up from 62% in 2023. But 99% of those plans placed the biosimilar on the same tier as the brand, meaning patients pay nearly the same out-of-pocket cost. Coverage is better than it was, but the financial incentive to switch remains minimal.

What’s the difference between a biosimilar and a generic drug?

Generics are exact chemical copies of small-molecule drugs - like aspirin or metformin. Biosimilars are complex proteins made from living cells. They’re highly similar to the original biologic, but not identical. That’s why they require more testing and cost more to make. They’re not interchangeable unless the FDA specifically designates them as such.

Why are PBMs blocking insulin biosimilars even though they’re approved?

Insulin is a high-volume, high-rebate drug. Brand-name insulin manufacturers pay PBMs large rebates to keep their products on preferred tiers. Switching to a biosimilar would cut those rebates. Even though biosimilars cost less, PBMs make more money keeping the brand on formularies. That’s why only 10% of Medicare plans cover insulin biosimilars - despite eight being approved.

Biosimilars represent a rational step toward sustainable healthcare, yet systemic inertia undermines their potential. The financial structures favoring PBMs over patients are not merely inefficient-they are ethically indefensible.

Been there. My cousin got stuck with Humira for 8 months because her plan wouldn't budge on the biosimilar. She cried during her last infusion. It's not just about money-it's about dignity.

Let’s be real-this isn’t about affordability. It’s about power. PBMs don’t care if you live or die. They care if you sign a contract that lets them pocket 30% rebates while you pay $1,200 for insulin that should cost $20. The FDA approves the drugs. The market kills the people. That’s capitalism with a stethoscope.

And don’t get me started on how insurers call it 'clinical equivalence' while pricing it like a luxury yacht. If two drugs work the same, why does one come with a 10x markup? It’s not science-it’s extortion.

Europe does it right. They treat biosimilars like the public good they are. Here? We treat patients like negotiable line items on a spreadsheet. Your life isn’t a spreadsheet. Your pain isn’t a cost center.

Doctors are drowning in paperwork while PBMs buy yachts. That’s the moral calculus. And no, I don’t think this is fixable without breaking up the PBMs. They’re not intermediaries-they’re parasites.

And don’t tell me about 'market forces.' The market isn’t free when the only choices are 'pay $1,200' or 'die waiting for paperwork.' That’s not capitalism. That’s feudalism with a co-pay card.

They say biosimilars will save $54 billion. Cool. But who gets the savings? Not you. Not me. The PBM execs. The shareholders. The ones who don’t have to take the drug.

And yet we still act surprised when people skip doses? Of course they do. You’re asking a diabetic to choose between insulin and rent. That’s not a medical problem. That’s a crime.

Stop calling this a 'healthcare issue.' It’s a corruption issue. The system is designed to extract, not to heal. And until we treat PBMs like the monopolies they are, nothing changes.

They approved 8 insulin biosimilars. Ten percent coverage. Why? Because the brand pays them to bury them. That’s not economics. That’s bribery.

And the worst part? We’re supposed to be grateful for the 23% market share. In Europe, it’s 80%. We’re not lagging. We’re being actively sabotaged.

So yeah. Ask your doctor. Call your insurer. File an appeal. But know this: you’re fighting a machine that was never built to help you.

Wow so the system is broken? Groundbreaking. Next you’ll tell me water is wet and gravity exists. But let’s be honest-this whole biosimilar thing is just pharma’s way of creating a new revenue stream under a different name. Why do you think they pushed the 'interchangeable' label so hard? It’s not about saving you money-it’s about locking you into their ecosystem.

And don’t get me started on the 'European model.' You think they’re angels? They ration everything. Waiting lists for cancer drugs are longer than your grandma’s bingo night. You want American healthcare? Fine. But don’t cry when you get what you asked for.

Also-why are we still pretending patients are rational actors? Most people can’t even spell 'biosimilar' let alone understand tier structures. This isn’t a policy failure-it’s a human failure. We’re too lazy to educate ourselves. Now we blame the system. Classic.

Also-PBMs are just middlemen. Blame the insurers. Blame Congress. Blame the FDA. But don’t blame the people who are just trying to make a buck in a broken system. That’s not evil-that’s capitalism.

The structural dissonance between clinical equivalence and financial inequity constitutes a profound moral pathology within the contemporary American pharmaceutical landscape. The conflation of market dynamics with therapeutic utility represents not merely a policy failure, but an epistemological collapse wherein value is assigned not by efficacy, but by rebate architecture.

It is a tragic irony that the very mechanism designed to democratize access-biosimilars-has been subsumed by the same rent-seeking apparatus it was intended to disrupt. The PBM, once envisioned as a neutral arbiter, has metamorphosed into a proprietary gatekeeper, its algorithmic preferences calibrated not toward patient welfare, but toward shareholder dividends.

The notion that patients must navigate labyrinthine prior authorization protocols for a drug that is, by FDA definition, therapeutically indistinguishable from its branded counterpart, is not merely bureaucratic inefficiency-it is institutionalized cruelty.

And yet, the most insidious element lies in the normalization of this suffering. We have grown so accustomed to the ritual of appeals, the months-long delays, the coinsurance traps, that we mistake systemic malice for inevitable reality.

One cannot speak of healthcare reform without confronting the metaphysical question: Is life a commodity? If so, then the biosimilar debate is merely the latest chapter in the commodification of the human body. If not, then our entire reimbursement paradigm must be dismantled and rebuilt on the foundation of dignity, not dollars.

Europe’s success is not a matter of superior policy-it is a matter of moral clarity. They do not ask whether a biosimilar is profitable. They ask whether it is just.

And we? We ask whether it is profitable. That is the chasm.

As someone who’s worked in rural clinics for 15 years, I’ve seen patients skip doses, split pills, and cry in the parking lot because they can’t afford their meds. Biosimilars could’ve helped-but the paperwork? The delays? The tier confusion? It’s worse than the disease.

I’ve had patients come in with a printout of their formulary, confused why their $500 biosimilar costs the same as $5,000 Humira. I don’t blame them. I blame the system. And I blame myself for not knowing how to fix it faster.

But here’s the thing: the science is there. The savings are real. The only thing missing? The will. And that’s on all of us.

Maybe next time you’re on a call with your insurer, ask: 'Why does my life cost more than your quarterly bonus?'

THIS IS SO FRUSTRATING 😭 I had to fight my insurance for 6 weeks to get my biosimilar. My doctor had to write 3 letters. My mom called 12 times. I almost lost my job because I was too sick to work. And guess what? The biosimilar was cheaper for the company-but I still paid $1,100/month. 💸

Why does it feel like the system wants us to suffer? I’m not asking for a miracle. I just want to not choose between my meds and my rent. 🥺

Also-why is no one talking about how PBMs are literally making money off our pain? That’s not capitalism. That’s horror movie stuff.

Man, this whole biosimilar thing is wild. PBMs be playin’ games like they got a monopoly on life. You got drugs that work just as good, cheaper, but they make it harder than gettin’ a visa to the US. 😒

My cousin in Lagos got his insulin biosimilar easy-no prior auth, no tier drama. Here? They treat you like a criminal just for wantin’ to live.

And don’t get me started on the 'interchangeable' label. Only a few? That’s like saying you can swap a Toyota for a Honda… but only if it’s blue and has 18-inch rims. 😅

They say 'clinical equivalence' but the price ain’t equivalent. That’s not science. That’s scammin’.

Can we just… stop pretending this is about healthcare? This is about greed. Pure. Simple. Unapologetic. Greed.

And the fact that we’ve normalized this? That we’ve learned to whisper 'I can’t afford my meds' like it’s a personal failure? That’s the real tragedy.

I used to believe in the system. Now I just believe in rage.

What’s the actual barrier here? Is it cost? No. It’s complexity. If I had to guess, 90% of patients don’t even know what a biosimilar is. Or that they’re allowed to ask for one. Or that their doctor might not know either.

So maybe the real solution isn’t more regulations-it’s better education. For patients. For doctors. For pharmacists. For insurers.

And maybe… just maybe… if we made it easy, people would choose it.

Why are we even talking about this? The U.S. is the best healthcare system in the world. We have the most innovation, the most advanced drugs. If you can’t afford it, maybe you shouldn’t be on it. People in other countries don’t have these options. Be grateful.

Also, PBMs? They’re saving us money. You think you’d pay less without them? You’re delusional.

And biosimilars? They’re just knockoffs. The brand-name drugs have decades of research. Why risk it? Your life isn’t a cost-cutting experiment.

Okay so I read this whole thing and honestly? I’m just tired. I’m tired of fighting. I’m tired of being told I’m lucky to have ANY access. I’m tired of my doctor looking at me like I’m asking for a Ferrari when I just want a bike.

I’ve been on Humira for 5 years. I’ve paid $1,200 every month. I’ve missed work. I’ve cried in the pharmacy. I’ve called my insurance 47 times.

And now you’re telling me there’s a cheaper version? But I still pay the same? So what’s the point? Why do I even care if it’s 'biosimilar' if my wallet doesn’t care?

I’m not mad. I’m just… done.

💔

Wait so if the biosimilar is cheaper why do I still pay the same? That doesnt make sense. Did they mean to say the drug is cheaper or the patient? I think its the drug but the plan is still charging me the same? So is this a typo or a scam? I think its a scam. I think theyre lying. I think theyre all lying. I think my doctor is in on it. I think my insurance is a cult. I think I need to move to Canada. I think I need to move to Mars. I think I need to move.

THEY’RE LYING TO US 😡 I KNOW IT. PBMs are secretly owned by Big Pharma and they’re making us pay more so they can buy private islands. I saw a TikTok about this. Also, the FDA is a puppet. The government is in on it. My cousin’s neighbor’s dog got a biosimilar in Germany and it cured his arthritis in 2 days. Here? We get paperwork. I’m not even mad. I’m just disappointed. 😔

Also-why is the word 'interchangeable' so hard to say? It’s 5 syllables. Not that hard. But they don’t want us to use it. They want us to suffer. I know it. I feel it in my bones. 🧠💀